Configurable 3MA with Crossover CloudThis script is a versatile and powerful enhancement of the classic triple moving average setup, designed to provide clear, at-a-glance insights into market trends and momentum shifts. It plots three moving averages on your chart and colors the area between the two shorter-term MAs, creating a visual "cloud" that instantly signals bullish or bearish sentiment.

The core of this indicator is its complete customizability, allowing you to tailor it precisely to your trading strategy and the asset you are analyzing.

Key Features:

Dynamic Crossover Cloud: The space between the first two moving averages is colored to represent momentum:

Green Cloud: Indicates a bullish crossover, where the shorter-term MA is above the medium-term MA.

Red Cloud: Indicates a bearish crossover, where the shorter-term MA is below the medium-term MA.

Complete Customization: Unlike standard MA indicators, every aspect of the three moving averages can be configured independently:

Length: Set the period for each MA.

Type: Choose between a Simple Moving Average (SMA) or an Exponential Moving Average (EMA) for each line.

Source: Base the calculation on any price source (close, open, high, low, hl2, etc.).

Individual Visibility Toggles: Clean up your chart by hiding any of the three moving averages directly from the settings panel.

How to Use:

This indicator is ideal for trend-following and crossover strategies.

Identify Momentum: Use the color of the cloud to quickly gauge short-term momentum. A green cloud suggests bullish strength, while a red cloud suggests bearish pressure.

Confirm the Trend: Use the third, long-term moving average (e.g., a 200-period MA) as a macro trend filter. For a higher probability trade, only consider long positions when the price is above the long-term MA and the cloud is green. Conversely, only consider short positions when the price is below the long-term MA and the cloud is red.

Customize for Your Style: Adjust the default settings (13 EMA, 50 SMA, 200 EMA) to fit your preferred timeframes and trading style, whether you're a scalper, day trader, or swing trader.

在腳本中搜尋"Exponential Moving Average"

On-Balance Volume with Multiple MA TypesOn-Balance Volume with Multiple MA Types

English Description

Overview

This is the first version of the "On-Balance Volume with Multiple MA Types" indicator designed to overlay directly on the price chart, a significant evolution from its previous iterations, which functioned solely as an oscillator in a separate window. The indicator calculates On-Balance Volume (OBV) and applies various smoothing methods to provide a clear view of volume dynamics in relation to price movements. It is pinned to the price scale for seamless integration with the chart.

Interpretation Recommendations

Price Pushing the OBV Line from Below: When the price chart pushes the OBV line upward and remains below it, this indicates rising volume, suggesting strong buying pressure.

Price Above the OBV Line: When the price chart is above the OBV line, it signals falling volume, indicating weakening momentum or selling pressure.

OBV Line Crossings: When the price crosses the OBV line, it represents a balance point in volume dynamics. The price level at the current crossing can be compared to the previous crossing to assess changes in market sentiment or momentum.

Moving Average Types

The indicator offers eight smoothing options for the OBV line, each with unique characteristics:

EMA (Exponential Moving Average): A weighted average that prioritizes recent data, providing a smooth yet responsive line.

DEMA (Double Exponential Moving Average): Uses two EMAs to reduce lag, offering faster response to volume changes.

HMA (Hull Moving Average): Combines weighted moving averages to minimize lag while maintaining smoothness.

WMA (Weighted Moving Average): Assigns more weight to recent data, balancing responsiveness and noise reduction.

TMA (Triangular Moving Average): A double-smoothed simple moving average, emphasizing central data points for smoother output.

VIDYA (Variable Index Dynamic Average): Adapts smoothing based on market volatility, using a CMO (Chande Momentum Oscillator) for dynamic weighting. Controlled by the VIDYA Alpha parameter (default: 0.2, range: 0–1), which adjusts sensitivity to volatility.

FRAMA (Fractal Adaptive Moving Average): Adjusts smoothing based on fractal dimensions of the OBV data, adapting to market conditions.

JMA (Jurik Moving Average): A proprietary adaptive average designed for minimal lag and high smoothness. Controlled by two parameters:

JMA Phase (default: 50, range: -100 to 100): Adjusts the balance between responsiveness and smoothness.

JMA Power (default: 1, range: 0.1+): Controls the strength of smoothing.

Input Parameters

OBV MA Length (default: 10): The lookback period for smoothing the OBV. Higher values produce smoother results but increase lag.

OBV MA Type (default: JMA): Selects the moving average type from the eight options listed above.

Line Width (default: 2): Thickness of the OBV line on the chart.

Bullish Color (default: Blue): Color of the OBV line when rising (indicating increasing volume).

Bearish Color (default: Red): Color of the OBV line when falling (indicating decreasing volume).

JMA Phase (default: 50): Adjusts the JMA’s responsiveness (used only when JMA is selected).

JMA Power (default: 1): Adjusts the JMA’s smoothing strength (used only when JMA is selected).

VIDYA Alpha (default: 0.2): Controls the sensitivity of VIDYA to market volatility (used only when VIDYA is selected).

How to Use

Add the indicator to your TradingView chart. It will overlay directly on the price chart, aligned with the price scale.

Adjust the OBV MA Type to select your preferred smoothing method based on your trading style (e.g., JMA for low lag, TMA for smoothness).

Modify the OBV MA Length to balance responsiveness and noise reduction. Shorter periods (e.g., 5–10) are better for short-term trading, while longer periods (e.g., 20–50) suit longer-term analysis.

Use the Bullish Color and Bearish Color to visually distinguish rising and falling volume trends.

For JMA or VIDYA, fine-tune the JMA Phase, JMA Power, or VIDYA Alpha to optimize the indicator for specific market conditions.

Interpret the OBV line in relation to price:

Watch for price pushing the OBV line upward (rising volume) or moving above it (falling volume).

Note crossings of the OBV line to identify balance points and compare with prior crossings to gauge momentum shifts.

Combine with other technical tools (e.g., support/resistance levels, trendlines) for a comprehensive trading strategy.

Notes

This indicator is designed to work on any timeframe and market, but its effectiveness depends on the chosen moving average type and parameters.

Experiment with different MA types and lengths to find the best fit for your trading approach.

The indicator is licensed under the Mozilla Public License 2.0 and copyrighted by TradingStrategyCourses © 2025.

Options Strategy V2.0📈 Options Strategy V2.0 – Intraday Reversal-Resilient Momentum System

Overview:

This strategy is designed specifically for intraday SPY, TSLA, MSFT, etc. options trading (0DTE or 1DTE), using high-probability signals derived from a confluence of technical indicators: EMA crossovers, RSI thresholds, ATR-based risk control, and volume spikes. The strategy aims to capture strong directional moves while avoiding overtrading, thanks to a built-in cooldown logic and optional time/session filters.

⚙️ Core Concept

The strategy executes trades only in the direction of the prevailing trend, determined by short- and long-term Exponential Moving Averages (EMA). Entry signals are generated when the Relative Strength Index (RSI) confirms momentum in the direction of the trend, and volume spikes suggest institutional activity.

To increase adaptability and user control, it includes a highly customizable parameter set for both long and short entries independently.

📌 Key Features

✅ Trend-Following Logic

Long entries are only allowed when EMA(short) > EMA(long)

Short entries are only allowed when EMA(short) < EMA(long)

✅ RSI Confirmation

Long: Requires RSI crossover above a configurable threshold

Short: Requires RSI crossunder below a configurable threshold

Optional rejection filters: Entry blocked above/below specific RSI extremes

✅ Volume Spike Filter

Confirms institutional participation by comparing current volume to an average multiplied by a user-defined factor.

✅ ATR-Based Risk Management

Both Stop Loss (SL) and Take Profit (TP) are dynamically calculated using ATR × a multiplier.

TP/SL ratio is fully configurable.

✅ Cooldown Control

After every trade, the system waits for a set number of bars before allowing new entries.

This prevents overtrading and increases signal quality.

Optionally, cooldown is ignored for reversal trades, ensuring the system can react immediately to a confirmed trend change.

✅ Candle Body Filter (Noise Control)

Avoids trades on candles with too small bodies relative to wicks (often noise or indecision candles).

✅ VWAP Confirmation (Optional)

Ensures price is trading above VWAP for long entries, or below for short entries.

✅ Time & Session Filters

Trades only during regular market hours (09:30–16:00 EST).

No-trade zone (e.g., 14:15–15:45 EST) to avoid low-liquidity traps or late-day whipsaws.

✅ End-of-Day Auto Close

All open positions are force-closed at 15:55 EST, protecting against overnight risk (especially relevant for 0DTE options).

📊 Visual Aids

EMA plots show trend direction

VWAP line provides real-time mean-reversion context

Stop Loss and Take Profit lines appear dynamically with each trade

Alerts notify of entry signals and exit triggers

🔧 Customization Panel

Nearly every element of the strategy can be tailored:

EMA lengths (short and long, for both sides)

RSI thresholds and length

ATR length, SL multiplier, and TP/SL ratio

Volume spike sensitivity

Minimum EMA distance filter

Candle body ratio filter

Session restrictions

Cooldown logic (duration + reversal exception)

This makes the strategy extremely versatile, allowing both conservative and aggressive configurations depending on the trader’s profile and the market context.

📌 Example Use Case: SPY Options (0DTE or 1DTE)

This system was designed and tested specifically for SPY and other intraday options trading, where:

Delta is around 0.50 or higher

Trades are short-lived (often 1–5 candles)

You aim to trade 1–3 signals per day, filtering out weak entries

🚫 Important Notes

It is not a scalping strategy; it relies on confirmed breakouts with trend support

No pyramiding or re-entries without cooldown to preserve risk integrity

Should be used with real-time alerts and manual broker execution

📈 Alerts Included

📈 Long Entry Signal

📉 Short Entry Signal

⚠️ Auto-closed all positions at 15:55 EST

✅ Proven Settings – Real Trades + Backtest Results

The current version of the strategy includes the optimal settings I’ve arrived at through extensive backtesting, as well as 3 months of real trading with consistent profitability. These results reflect real-world execution under live market conditions using 0DTE SPY options, with disciplined trade management and risk control.

🧠 Final Thoughts

Options Strategy V2.0 is a robust, highly tunable intraday strategy that blends momentum, trend-following, and volume confirmation. It is ideal for disciplined traders focused on SPY or other 0DTE/1DTE options, and it includes guardrails to reduce false signals and improve execution timing.

Perfect for those who seek precision, flexibility, and risk-defined setups—not blind automation.

Logarithmic Moving Average (LMA) [QuantAlgo]🟢 Overview

The Logarithmic Moving Average (LMA) uses advanced logarithmic weighting to create a dynamic trend-following indicator that prioritizes recent price action while maintaining statistical significance. Unlike traditional moving averages that use linear or exponential weights, this indicator employs logarithmic decay functions to create a more sophisticated price averaging system that adapts to market volatility and momentum conditions.

The indicator displays a smoothed signal line that oscillates around zero, with positive values indicating bullish momentum and negative values indicating bearish momentum. The signal incorporates trend quality assessment, momentum confirmation, and multiple filtering mechanisms to help traders and investors identify trend continuation and reversal opportunities across different timeframes and asset classes.

🟢 How It Works

The indicator's core innovation lies in its logarithmic weighting system, where weights are calculated using the formula: w = 1.0 / math.pow(math.log(i + steepness), 2) The steepness parameter controls how aggressively recent data is prioritized over historical data, creating a dynamic weight decay that can be fine-tuned for different trading styles. This logarithmic approach provides more nuanced weight distribution compared to exponential moving averages, offering better responsiveness while maintaining stability.

The LMA calculation combines multiple sophisticated components. First, it calculates the logarithmic weighted average of closing prices. Then it measures the slope of this average over a 10-period lookback: lmaSlope = (lma - lma ) / lma * 100 The system also incorporates trend quality assessment using R-squared correlation analysis of log-transformed prices, measuring how well the price data fits a linear trend model over the specified period.

The final signal generation uses the formula: signal = lmaSlope * (0.5 + rSquared * 0.5) which combines the LMA slope with trend quality weighting. When momentum confirmation is enabled, the indicator calculates annualized log-return momentum and applies a multiplier when the momentum direction aligns with the signal direction, strengthening confirmed signals while filtering out weak or counter-trend movements.

🟢 How to Use

1. Signal Interpretation and Threshold Zones

Positive Values (Above Zero): LMA slope indicating bullish momentum with upward price trajectory relative to logarithmic baseline

Negative Values (Below Zero): LMA slope indicating bearish momentum with downward price trajectory relative to logarithmic baseline

Zero Line Crosses: Signal transitions between bullish and bearish regimes, indicating potential trend changes

Long Entry Threshold Zone: Area above positive threshold (default 0.5) indicating confirmed bullish signals suitable for long positions

Short Entry Threshold Zone: Area below negative threshold (default -0.5) indicating confirmed bearish signals suitable for short positions

Extreme Values: Signals exceeding ±1.0 represent strong momentum conditions with higher probability of continuation

2. Momentum Confirmation and Visual Analysis

Signal Color Intensity: Gradient coloring shows signal strength, with brighter colors indicating stronger momentum

Bar Coloring: Optional price bar coloring matches signal direction for quick visual trend identification

Position Labels: Real-time position classification (Bullish/Bearish/Neutral) displayed on the latest bar

Momentum Weight Factor: When short-term log-return momentum aligns with LMA signal direction, the signal receives additional weight confirmation

Trend Quality Component: R-squared values weight the signal strength, with higher correlation indicating more reliable trend conditions

3. Examples: Preconfigured Settings

Default: Universally applicable configuration balanced for medium-term investing and general trading across multiple timeframes and asset classes.

Scalping: Highly responsive setup with shorter period and higher steepness for ultra-short-term trades on 1-15 minute charts, optimized for quick momentum shifts.

Swing Trading: Extended period with moderate steepness and increased smoothing for multi-day positions, designed to filter noise while capturing larger price swings on 1-4 hour and daily charts.

Trend Following: Maximum smoothing with lower steepness for established trend identification, generating fewer but more reliable signals optimal for daily and weekly timeframes.

Mean Reversion: Shorter period with high steepness for counter-trend strategies, more sensitive to extreme moves and reversal opportunities in ranging market conditions.

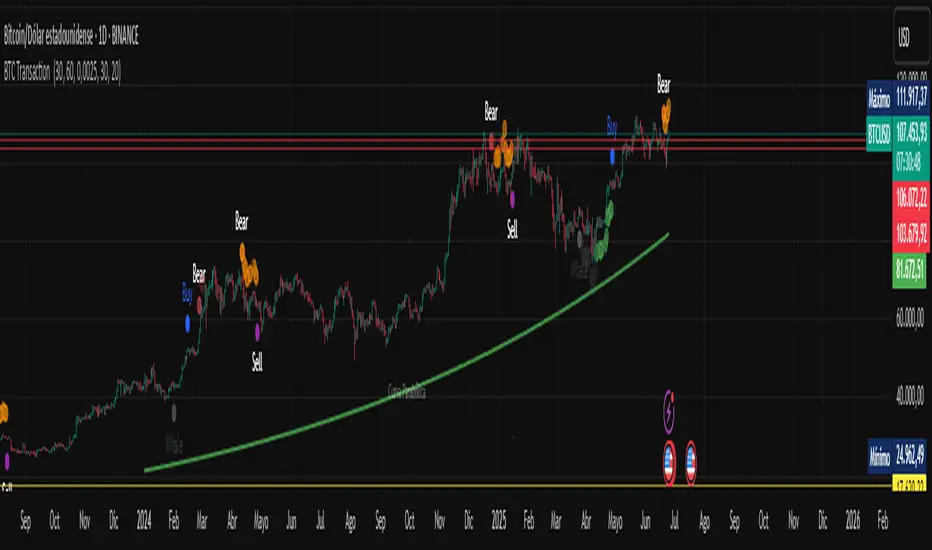

BTC Transaction Indicator Name: "Bitcoin On-Chain Volume & Dynamic Parabolic Curve Signals"

Purpose:

This indicator is designed for Bitcoin traders and long-term holders. It combines the analysis of Bitcoin's on-chain transaction volume with price action to generate "Whale" and "Bear" signals. Additionally, it features a unique dynamic parabolic curve that acts as a visual support line, adapting its visibility based on price interaction with a key Exponential Moving Average (EMA).

Key Components:

On-Chain Volume Analysis:

Utilizes Estimated Transaction Volume (ETRAV) data from the Bitcoin blockchain.

Calculates fast and slow Simple Moving Averages (SMAs) of this volume.

Identifies volume trends (up/down) and significant volume increases/decreases.

Employs fixed thresholds (2,500,000 for low volume and 25,000,000 for high volume) to define key activity levels, similar to how historical on-chain analysis defined accumulation and distribution zones.

Price Action Analysis:

Calculates fast and slow SMAs of the price.

Detects price trends (up/down), recoveries, and declines based on these price SMAs.

"Whale" and "Bear" Signals:

Whale Signals (Buy-side): Generated when there's an upward volume trend, significant volume increase, and a downward price trend followed by price recovery. These indicate potential accumulation phases.

Bear Signals (Sell-side): Generated when there's a downward volume trend, significant volume decrease, and an upward price trend followed by price decline. These indicate potential distribution phases.

Visuals: Both types of signals are plotted as small, colored circles directly on the price chart, with corresponding text labels ("Whale," "Buy," "Bear," "Sell," "Price Recovering," "Price Declining").

Dynamic Parabolic Curve:

Concept: A green parabolic (exponential) curve that serves as a dynamic visual support line.

Activation: The curve starts drawing automatically only when the price crosses over the EMA 500 (Exponential Moving Average of 500 periods). The curve's starting point is set at a user-defined percentage below the EMA 500 value at that exact crossover point.

Visibility: The curve remains visible and continues its trajectory only as long as the price stays above the EMA 500.

Deactivation: The curve disappears instantly if the price falls below or equals the EMA 500. It will only reappear if the price crosses above the EMA 500 again.

Customization: The curve's steepness (Tasa Crecimiento Curva) and its initial distance from the EMA 500 (Inicio Curva % por debajo de EMA500) are adjustable.

Dynamic Label: A "Parabólico" text label is plotted near the center of the active curve segment, with an adjustable vertical offset to ensure it stays visually appealing below the curve.

What is PLOTTED on the chart:

The small, colored circle signals for Whale/Buy and Bear/Sell activity.

The green dynamic parabolic curve.

What is NOT PLOTTED:

EMA 200, EMA 500 lines (though they are calculated internally for logic).

Raw volume data or volume Moving Averages (these are only used for signal calculation, not plotted).

Ideal for:

Bitcoin traders and investors focused on long-term trends and cycle analysis, who want visual cues for accumulation/distribution phases based on on-chain activity, complemented by a unique, dynamically appearing parabolic support curve.

Important Notes:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe for optimal on-chain data relevance.

Super MTF Clouds (4x3 Pairs)Overview:

This script is based on Ripster's MTF clouds, which transcends the standard moving average cloud indicator by offering a powerful and deeply customizable Multi-Timeframe (MTF) analysis. Instead of being limited to the moving averages of your current charts from the current timeframe, this tool allows you to project and visualize the trend and key support/resistance zones from up to 4 different timeframes simultaneously. User can input up to 6 different EMA values which will form 3 pairs of EMA clouds, for each of the timeframes.

The primary purpose is to provide traders with immediate confluence. By observing how price interacts with moving average clouds from higher timeframes (e.g., Hourly, Daily, Weekly), you can make more informed decisions on your active trading timeframe (e.g., 10 Minute). It's designed as a complete MTF Cloud toolkit, allowing you to display all necessary MTFs in a single script to build a comprehensive view of the market structure without having to flick to different timeframe to look for cloud positions.

Key features:

Four Independent Multi-Timeframe Slots: Each slot can be assigned any timeframe available on TradingView (e.g., D, W, M, 4H).

Three MA Pairs Per Timeframe: For each timeframe, configure up to three separate MA clouds (e.g., a 9/12 EMA pair, a 20/50 EMA pair, and a 100/200 SMA pair).

Complete Customisation: For every single moving average (24 in total), you can independently control:

MA Type: Choose between EMA or SMA.

Length: Any period you require.

Line Color: Full colour selection.

Line Thickness: Adjust the visual weight of each line.

Cloud Control: For every pair (12 in total), you can set the fill colour and transparency.

How To Use This Script:

This tool is best used for confirmation and context. Here are some practical strategies that one can adopt:

Trend Confluence: Before taking a trade based on a signal on your current timeframe, glance at the higher timeframe clouds. If you see a buy signal on the 15-minute chart and the price is currently trading above a thick, bullish Daily cloud, the probability of that trade succeeding is significantly higher. Conversely, shorting into strong HTF support is a low-probability trade.

Dynamic Support & Resistance: The edges of the higher timeframe clouds often act as powerful, dynamic levels of support and resistance. A pullback to the 4-Hour 50 EMA on your 15-minute chart can be a prime area to look for entries in the direction of the larger trend.

Gauging Market Regimes: Use the toggles in the settings to quickly switch between different views. You can have a "risk-on" view with short-term clouds and a "macro" view with weekly and monthly clouds. This helps you adapt your trading style to the current market conditions.

Key Settings:

1. Global Setting

Source For All MAs: This determines the price data point used for every single moving average calculation.

Default: hl2 (an average of the High and Low of each bar). This gives a smooth midpoint price.

Options: You can change this to Close (the most common method), Open, High, Low, or ohlc4 (an average of the open, high, low, and close), among others.

Recommendation: For most standard trend analysis, the default hl2 is the common choice.

2. The Timeframe Group Structure

The rest of the settings are organized into four identical, collapsible groups: "Timeframe 1 Settings" through "Timeframe 4 Settings". Each group acts as a self-contained control panel for one multi-timeframe view.

Within each timeframe group, you have two master controls:

Enable Timeframe: This is the main power switch for the entire group. Uncheck this box to instantly hide all three clouds and lines associated with this timeframe. This is perfect for quickly decluttering your chart or focusing on a different set of analyses.

Timeframe: This dropdown menu is the heart of the MTF feature. Here, you select the higher timeframe you want to analyse (e.g., 1D for Daily, 1W for Weekly, 4H for 4-Hour). All calculations for the three pairs within this group will be based on the timeframe you select here.

3. Pair-Specific Controls

Inside each timeframe group, there are three sections for "Pair 1", "Pair 2", and "Pair 3". These control each individual moving average cloud.

Enable Pair: Just like the master switch for the timeframe, this checkbox turns a single cloud and its two MA lines on or off.

For each pair, the settings are further broken down:

Moving Average Lines (A and B): These two rows control the two moving averages that form the cloud. 'A' is typically used for the shorter-period MA and 'B' for the longer-period one.

Type (A/B): A dropdown menu to select either EMA (Exponential Moving Average) or SMA (Simple Moving Average). EMAs react more quickly to recent price changes, while SMAs are smoother and react more slowly.

Length (A/B): The lookback period for the moving average (e.g., 21, 50, 200).

Color (A/B): Sets the specific colour of the MA line itself on your chart.

Cloud Fill Settings

Fill Color: This controls the colour of the shaded area (the "cloud") between the two moving average lines. For a consistent look, you can set this to the same colour as your shorter MA line.

Transparency: Controls how see-through the cloud is, on a scale of 0 to 100. 0 is a solid, opaque colour, while 100 is completely invisible. The default of 85 provides a light, "cloud-like" appearance that doesn't obscure the price action.

----------------------------------------------------------------------

If anything is not clear please let me know!

Multi-Indicator Trend-Following Strategy v6Multi-Indicator Trend-Following Strategy v6

This strategy uses a combination of technical indicators to identify potential trend-following trade entries and exits. It is intended for educational and research purposes.

How it works:

Moving Averages (EMA): Entry signals are generated on crossovers between a fast and slow exponential moving average.

RSI Filter: Confirms momentum with a threshold above/below 50 for long/short entries.

Volume Confirmation: Requires volume to exceed a moving average multiplied by a user-defined factor.

ATR-Based Risk Management: Stop loss and take profit levels are calculated using the Average True Range (ATR), allowing for dynamic risk control based on market volatility.

Customizable Inputs:

Fast/Slow MA lengths

RSI length and levels

MACD settings (used in calculation, not directly in signal)

Volume MA and multiplier

ATR period and multipliers for stop loss and take profit

Notes:

This strategy does not guarantee future results.

It is provided for analysis and backtesting only.

Alerts are available for buy/sell conditions.

Feel free to adjust parameters to explore different market conditions and asset classes.

C&B Auto MK5C&B Auto MK5.2ema BullBear

Overview

The C&B Auto MK5.2ema BullBear is a versatile Pine Script indicator designed to help traders identify bullish and bearish market conditions across various timeframes. It combines Exponential Moving Averages (EMAs), Relative Strength Index (RSI), Average True Range (ATR), and customizable time filters to generate actionable signals. The indicator overlays on the price chart, displaying EMAs, a dynamic cloud, scaled RSI levels, bull/bear signals, and market condition labels, making it suitable for swing trading, day trading, or scalping in trending or volatile markets.

What It Does

This indicator generates bull and bear signals based on the interaction of two EMAs, filtered by RSI thresholds, ATR-based volatility, a 50/200 EMA trend filter, and user-defined time windows. It adapts to market volatility by adjusting EMA lengths and RSI thresholds. A dynamic cloud highlights trend direction or neutral zones, with candlestick coloring in neutral conditions. Market condition labels (current and historical) provide real-time trend and volatility context, displayed above the chart.

How It Works

The indicator uses the following components:

EMAs: Two EMAs (short and long) are calculated on a user-selected timeframe (1, 5, 15, 30, or 60 minutes). Their crossover or crossunder triggers potential bull/bear signals. EMA lengths adjust based on volatility (e.g., 10/20 for volatile markets, 5/10 for non-volatile).

Dynamic Cloud: The area between the EMAs forms a cloud, colored green for bullish trends, red for bearish trends, or a user-defined color (default yellow) for neutral zones (when EMAs are close, determined by an ATR-based threshold). Users can widen the cloud for visibility.

RSI Filter: RSI is scaled to price levels and plotted on the chart (optional). Signals are filtered to ensure RSI is within volatility-adjusted bull/bear thresholds and not in overbought/oversold zones.

ATR Volatility Filter: An optional filter ensures signals occur during sufficient volatility (ATR(14) > SMA(ATR, 20)).

50/200 EMA Trend Filter: An optional filter restricts bull signals to bullish trends (50 EMA > 200 EMA) and bear signals to bearish trends (50 EMA < 200 EMA).

Time Filter: Signals are restricted to a user-defined UTC time window (default 9:00–15:00), aligning with active trading sessions.

Market Condition Labels: Labels above the chart display the current trend (Bullish, Bearish, Neutral) and optionally volatility (e.g., “Bullish Volatile”). Up to two historical labels persist for a user-defined number of bars (default 5) to show recent trend changes.

Visual Aids: Bull signals appear as green triangles/labels below the bar, bear signals as red triangles/labels above. Candlesticks in neutral zones are colored (default yellow).

The indicator ensures compatibility with standard chart types (e.g., candlestick or bar charts) to produce realistic signals, avoiding non-standard types like Heikin Ashi or Renko.

How to Use It

Add to Chart: Apply the indicator to a candlestick or bar chart on TradingView.

Configure Settings:

Timeframe: Choose a timeframe (1, 5, 15, 30, or 60 minutes) to match your trading style.

Filters:

Enable/disable the ATR volatility filter to focus on high-volatility periods.

Enable/disable the 50/200 EMA trend filter to align signals with the broader trend.

Enable the time filter and set custom UTC hours/minutes (default 9:00–15:00).

Cloud Settings: Adjust the cloud width, neutral zone threshold, color, and transparency.

EMA Colors: Use default trend-based colors or set custom colors for short/long EMAs.

RSI Display: Toggle the scaled RSI and its thresholds, with customizable colors.

Signal Settings: Toggle bull/bear labels and set signal colors.

Market Condition Labels: Toggle current/historical labels, include/exclude volatility, and adjust decay period.

Interpret Signals:

Bull Signal: A green triangle or “Bull” label below the bar indicates potential bullish momentum (EMA crossover, RSI above bull threshold, within time window, passing filters).

Bear Signal: A red triangle or “Bear” label above the bar indicates potential bearish momentum (EMA crossunder, RSI below bear threshold, within time window, passing filters).

Neutral Zone: Yellow candlesticks and cloud (if enabled) suggest a lack of clear trend; consider range-bound strategies or avoid trading.

Market Condition Labels: Check labels above the chart for real-time trend (Bullish, Bearish, Neutral) and volatility status to confirm market context.

Monitor Context: Use the cloud, RSI, and labels to assess trend strength and volatility before acting on signals.

Unique Features

Volatility-Adaptive EMAs: Automatically adjusts EMA lengths based on ATR to suit volatile or non-volatile markets, reducing manual configuration.

Neutral Zone Detection: Uses an ATR-based threshold to identify low-trend periods, helping traders avoid choppy markets.

Scaled RSI Visualization: Plots RSI and thresholds directly on the price chart, simplifying momentum analysis relative to price.

Flexible Time Filtering: Supports precise UTC-based trading windows, ideal for day traders targeting specific sessions.

Historical Market Labels: Displays recent trend changes (up to two) with a decay period, providing context for market shifts.

50/200 EMA Trend Filter: Aligns signals with the broader market trend, enhancing signal reliability.

Notes

Use on standard candlestick or bar charts to ensure accurate signals.

Test the indicator on a demo account to optimize settings for your market and timeframe.

Combine with other analysis (e.g., support/resistance, volume) for better decision-making.

The indicator is not a standalone system; use it as part of a broader trading strategy.

Limitations

Signals may lag in fast-moving markets due to EMA-based calculations.

Neutral zone detection may vary in extremely volatile or illiquid markets.

Time filters are UTC-based; ensure your platform’s timezone settings align.

This indicator is designed for traders seeking a customizable, trend-following tool that adapts to volatility and provides clear visual cues with robust filtering for bullish and bearish market conditions.

[SM-042] EMA 5-8-13 with ADX FilterWhat is the strategy?

The strategy combines three exponential moving averages (EMAs) — 5, 8, and 13 periods — with an optional ADX (Average Directional Index) filter. It is designed to enter long or short positions based on EMA crossovers and to exit positions when the price crosses a specific EMA. The ADX filter, if enabled, adds a condition that only allows trades when the ADX value is above a certain threshold, indicating trend strength.

Who is it for?

This strategy is for traders leveraging EMAs and trend strength indicators to make trade decisions. It can be used by anyone looking for a simple trend-following strategy, with the flexibility to adjust for trend strength using the ADX filter.

When is it used?

- **Long trades**: When the 5-period EMA crosses above the 8-period EMA, with an optional ADX condition (if enabled) that requires the ADX value to be above a specified threshold.

- **Short trades**: When the 5-period EMA crosses below the 8-period EMA, with the ADX filter again optional.

- **Exits**: The strategy exits a long position when the price falls below the 13-period EMA and exits a short position when the price rises above the 13-period EMA.

Where is it applied?

This strategy is applied on a chart with any asset on TradingView, with the EMAs and ADX plotted for visual reference. The strategy uses `strategy.entry` to open positions and `strategy.close` to close them based on the set conditions.

Why is it useful?

This strategy helps traders identify trending conditions and filter out potential false signals by using both EMAs (to capture short-term price movements) and the ADX (to confirm the strength of the trend). The ADX filter can be turned off if not desired, making the strategy flexible for both trending and range-bound markets.

How does it work?

- **EMA Crossover**: The strategy enters a long position when the 5-period EMA crosses above the 8-period EMA, and enters a short position when the 5-period EMA crosses below the 8-period EMA.

- **ADX Filter**: If enabled, the strategy checks whether the ADX value is above a set threshold (default is 20) before allowing a trade.

- **Exit Conditions**: Long positions are closed when the price falls below the 13-period EMA, and short positions are closed when the price rises above the 13-period EMA.

- **Plotting**: The strategy plots the three EMAs and the ADX value on the chart for visualization. It also displays a horizontal line at the ADX threshold.

This setup allows for clear decision-making based on the interaction between different time-frame EMAs and trend strength as indicated by ADX.

Multi-Fibonacci Trend Average[FibonacciFlux]Multi-Fibonacci Trend Average (MFTA): An Institutional-Grade Trend Confluence Indicator for Discerning Market Participants

My original indicator/Strategy:

Engineered for the sophisticated demands of institutional and advanced traders, the Multi-Fibonacci Trend Average (MFTA) indicator represents a paradigm shift in technical analysis. This meticulously crafted tool is designed to furnish high-definition trend signals within the complexities of modern financial markets. Anchored in the rigorous principles of Fibonacci ratios and augmented by advanced averaging methodologies, MFTA delivers a granular perspective on trend dynamics. Its integration of Multi-Timeframe (MTF) filters provides unparalleled signal robustness, empowering strategic decision-making with a heightened degree of confidence.

MFTA indicator on BTCUSDT 15min chart with 1min RSI and MACD filters enabled. Note the refined signal generation with reduced noise.

MFTA indicator on BTCUSDT 15min chart without MTF filters. While capturing more potential trading opportunities, it also generates a higher frequency of signals, including potential false positives.

Core Innovation: Proprietary Fibonacci-Enhanced Supertrend Averaging Engine

The MFTA indicator’s core innovation lies in its proprietary implementation of Supertrend analysis, strategically fortified by Fibonacci ratios to construct a truly dynamic volatility envelope. Departing from conventional Supertrend methodologies, MFTA autonomously computes not one, but three distinct Supertrend lines. Each of these lines is uniquely parameterized by a specific Fibonacci factor: 0.618 (Weak), 1.618 (Medium/Golden Ratio), and 2.618 (Strong/Extended Fibonacci).

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval=0.01, step=0.01, tooltip='Factor 1 (Weak/Fibonacci)', group="Fibonacci Supertrend")

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval=0.01, step=0.01, tooltip='Factor 2 (Medium/Golden Ratio)', group="Fibonacci Supertrend")

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval=0.01, step=0.01, tooltip='Factor 3 (Strong/Extended Fib)', group="Fibonacci Supertrend")

This multi-faceted architecture adeptly captures a spectrum of market volatility sensitivities, ensuring a comprehensive assessment of prevailing conditions. Subsequently, the indicator algorithmically synthesizes these disparate Supertrend lines through arithmetic averaging. To achieve optimal signal fidelity and mitigate inherent market noise, this composite average is further refined utilizing an Exponential Moving Average (EMA).

// Calculate average of the three supertends and a smoothed version

superlength = input.int(21, 'Smoothing Length', tooltip='Smoothing Length for Average Supertrend', group="Fibonacci Supertrend")

average_trend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_trend = ta.ema(average_trend, superlength)

The resultant ‘Smoothed Trend’ line emerges as a remarkably responsive yet stable trend demarcation, offering demonstrably superior clarity and precision compared to singular Supertrend implementations, particularly within the turbulent dynamics of high-volatility markets.

Elevated Signal Confluence: Integrated Multi-Timeframe (MTF) Validation Suite

MFTA transcends the limitations of conventional trend indicators by incorporating an advanced suite of three independent MTF filters: RSI, MACD, and Volume. These filters function as sophisticated validation protocols, rigorously ensuring that only signals exhibiting a confluence of high-probability factors are brought to the forefront.

1. Granular Lower Timeframe RSI Momentum Filter

The Relative Strength Index (RSI) filter, computed from a user-defined lower timeframe, furnishes critical momentum-based signal validation. By meticulously monitoring RSI dynamics on an accelerated timeframe, traders gain the capacity to evaluate underlying momentum strength with precision, prior to committing to signal execution on the primary chart timeframe.

// --- Lower Timeframe RSI Filter ---

ltf_rsi_filter_enable = input.bool(false, title="Enable RSI Filter", group="MTF Filters", tooltip="Use RSI from lower timeframe as a filter")

ltf_rsi_timeframe = input.timeframe("1", title="RSI Timeframe", group="MTF Filters", tooltip="Timeframe for RSI calculation")

ltf_rsi_length = input.int(14, title="RSI Length", minval=1, group="MTF Filters", tooltip="Length for RSI calculation")

ltf_rsi_threshold = input.int(30, title="RSI Threshold", minval=0, maxval=100, group="MTF Filters", tooltip="RSI value threshold for filtering signals")

2. Convergent Lower Timeframe MACD Trend-Momentum Filter

The Moving Average Convergence Divergence (MACD) filter, also calculated on a lower timeframe basis, introduces a critical layer of trend-momentum convergence confirmation. The bullish signal configuration rigorously mandates that the MACD line be definitively positioned above the Signal line on the designated lower timeframe. This stringent condition ensures a robust indication of converging momentum that aligns synergistically with the prevailing trend identified on the primary timeframe.

// --- Lower Timeframe MACD Filter ---

ltf_macd_filter_enable = input.bool(false, title="Enable MACD Filter", group="MTF Filters", tooltip="Use MACD from lower timeframe as a filter")

ltf_macd_timeframe = input.timeframe("1", title="MACD Timeframe", group="MTF Filters", tooltip="Timeframe for MACD calculation")

ltf_macd_fast_length = input.int(12, title="MACD Fast Length", minval=1, group="MTF Filters", tooltip="Fast EMA length for MACD")

ltf_macd_slow_length = input.int(26, title="MACD Slow Length", minval=1, group="MTF Filters", tooltip="Slow EMA length for MACD")

ltf_macd_signal_length = input.int(9, title="MACD Signal Length", minval=1, group="MTF Filters", tooltip="Signal SMA length for MACD")

3. Definitive Volume Confirmation Filter

The Volume Filter functions as an indispensable arbiter of trade conviction. By establishing a dynamic volume threshold, defined as a percentage relative to the average volume over a user-specified lookback period, traders can effectively ensure that all generated signals are rigorously validated by demonstrably increased trading activity. This pivotal validation step signifies robust market participation, substantially diminishing the potential for spurious or false breakout signals.

// --- Volume Filter ---

volume_filter_enable = input.bool(false, title="Enable Volume Filter", group="MTF Filters", tooltip="Use volume level as a filter")

volume_threshold_percent = input.int(title="Volume Threshold (%)", defval=150, minval=100, group="MTF Filters", tooltip="Minimum volume percentage compared to average volume to allow signal (100% = average)")

These meticulously engineered filters operate in synergistic confluence, requiring all enabled filters to definitively satisfy their pre-defined conditions before a Buy or Sell signal is generated. This stringent multi-layered validation process drastically minimizes the incidence of false positive signals, thereby significantly enhancing entry precision and overall signal reliability.

Intuitive Visual Architecture & Actionable Intelligence

MFTA provides a demonstrably intuitive and visually rich charting environment, meticulously delineating trend direction and momentum through precisely color-coded plots:

Average Supertrend: Thin line, green/red for uptrend/downtrend, immediate directional bias.

Smoothed Supertrend: Bold line, teal/purple for uptrend/downtrend, cleaner, institutionally robust trend.

Dynamic Trend Fill: Green/red fill between Supertrends quantifies trend strength and momentum.

Adaptive Background Coloring: Light green/red background mirrors Smoothed Supertrend direction, holistic trend perspective.

Precision Buy/Sell Signals: ‘BUY’/‘SELL’ labels appear on chart when trend touch and MTF filter confluence are satisfied, facilitating high-conviction trade action.

MFTA indicator applied to BTCUSDT 4-hour chart, showcasing its effectiveness on higher timeframes. The Smoothed Length parameter is increased to 200 for enhanced smoothness on this timeframe, coupled with 1min RSI and Volume filters for signal refinement. This illustrates the indicator's adaptability across different timeframes and market conditions.

Strategic Applications for Institutional Mandates

MFTA’s sophisticated design provides distinct advantages for advanced trading operations and institutional investment mandates. Key strategic applications include:

High-Probability Trend Identification: Fibonacci-averaged Supertrend with MTF filters robustly identifies high-probability trend continuations and reversals, enhancing alpha generation.

Precision Entry/Exit Signals: Volume and momentum-filtered signals enable institutional-grade precision for optimized risk-adjusted returns.

Algorithmic Trading Integration: Clear signal logic facilitates seamless integration into automated trading systems for scalable strategy deployment.

Multi-Asset/Timeframe Versatility: Adaptable parameters ensure applicability across diverse asset classes and timeframes, catering to varied trading mandates.

Enhanced Risk Management: Superior signal fidelity from MTF filters inherently reduces false signals, supporting robust risk management protocols.

Granular Customization and Parameterized Control

MFTA offers unparalleled customization, empowering users to fine-tune parameters for precise alignment with specific trading styles and market conditions. Key adjustable parameters include:

Fibonacci Factors: Adjust Supertrend sensitivity to volatility regimes.

ATR Length: Control volatility responsiveness in Supertrend calculations.

Smoothing Length: Refine Smoothed Trend line responsiveness and noise reduction.

MTF Filter Parameters: Independently configure timeframes, lookback periods, and thresholds for RSI, MACD, and Volume filters for optimal signal filtering.

Disclaimer

MFTA is meticulously engineered for high-quality trend signals; however, no indicator guarantees profit. Market conditions are unpredictable, and trading involves substantial risk. Rigorous backtesting and forward testing across diverse datasets, alongside a comprehensive understanding of the indicator's logic, are essential before live deployment. Past performance is not indicative of future results. MFTA is for informational and analytical purposes only and is not financial or investment advice.

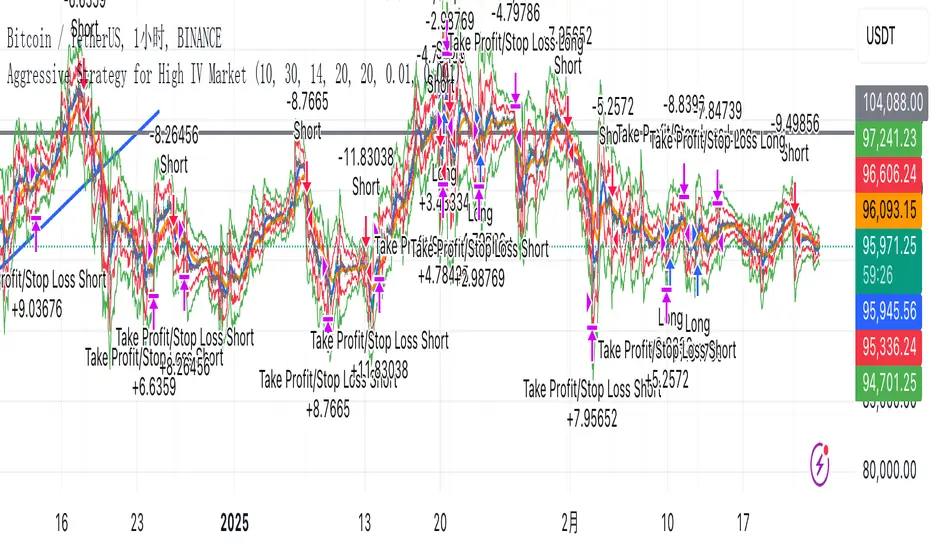

Aggressive Strategy for High IV Market### Strategic background

In a volatile high IV market, prices are volatile and market expectations of future uncertainty are high. This environment provides opportunities for aggressive trading strategies, but also comes with a high level of risk. In pursuit of a high Sharpe ratio (i.e., risk-adjusted return), we need to design a strategy that captures the benefits of market volatility while effectively controlling risk. Based on daily line cycles, I choose a combination of trend tracking and volatility filtering for highly volatile assets such as stocks, futures or cryptocurrencies.

---

### Strategy framework

#### Data

- Use daily data, including opening, closing, high and low prices.

- Suitable for highly volatile markets such as technology stocks, cryptocurrencies or volatile index futures.

#### Core indicators

1. ** Trend Indicators ** :

Fast Exponential Moving Average (EMA_fast) : 10-day EMA, used to capture short-term trends.

- Slow Exponential Moving Average (EMA_slow) : 30-day EMA, used to determine the long-term trend.

2. ** Volatility Indicators ** :

Average true Volatility (ATR) : 14-day ATR, used to measure market volatility.

- ATR mean (ATR_mean) : A simple moving average of the 20-day ATR that serves as a volatility benchmark.

- ATR standard deviation (ATR_std) : The standard deviation of the 20-day ATR, which is used to judge extreme changes in volatility.

#### Trading logic

The strategy is based on a trend following approach of double moving averages and filters volatility through ATR indicators, ensuring that trading only in a high-volatility environment is in line with aggressive and high sharpe ratio goals.

---

### Entry and exit conditions

#### Admission conditions

- ** Multiple entry ** :

- EMA_fast Crosses EMA_slow (gold cross), indicating that the short-term trend is turning upward.

-ATR > ATR_mean + 1 * ATR_std indicates that the current volatility is above average and the market is in a state of high volatility.

- ** Short Entry ** :

- EMA_fast Crosses EMA_slow (dead cross) downward, indicating that the short-term trend turns downward.

-ATR > ATR_mean + 1 * ATR_std, confirming high volatility.

#### Appearance conditions

- ** Long show ** :

- EMA_fast Enters the EMA_slow (dead cross) downward, and the trend reverses.

- or ATR < ATR_mean-1 * ATR_std, volatility decreases significantly and the market calms down.

- ** Bear out ** :

- EMA_fast Crosses the EMA_slow (gold cross) on the top, and the trend reverses.

- or ATR < ATR_mean-1 * ATR_std, the volatility is reduced.

---

### Risk management

To control the high risk associated with aggressive strategies, set up the following mechanisms:

1. ** Stop loss ** :

- Long: Entry price - 2 * ATR.

- Short: Entry price + 2 * ATR.

- Dynamic stop loss based on ATR can adapt to market volatility changes.

2. ** Stop profit ** :

- Fixed profit target can be selected (e.g. entry price ± 4 * ATR).

- Or use trailing stop losses to lock in profits following price movements.

3. ** Location Management ** :

- Reduce positions appropriately in times of high volatility, such as dynamically adjusting position size according to ATR, ensuring that the risk of a single trade does not exceed 1%-2% of the account capital.

---

### Strategy features

- ** Aggressiveness ** : By trading only in a high ATR environment, the strategy takes full advantage of market volatility and pursues greater returns.

- ** High Sharpe ratio potential ** : Trend tracking combined with volatility filtering to avoid ineffective trades during periods of low volatility and improve the ratio of return to risk.

- ** Daily line Cycle ** : Based on daily line data, suitable for traders who operate frequently but are not too complex.

---

### Implementation steps

1. ** Data Preparation ** :

- Get the daily data of the target asset.

- Calculate EMA_fast (10 days), EMA_slow (30 days), ATR (14 days), ATR_mean (20 days), and ATR_std (20 days).

2. ** Signal generation ** :

- Check EMA cross signals and ATR conditions daily to generate long/short signals.

3. ** Execute trades ** :

- Enter according to the signal, set stop loss and profit.

- Monitor exit conditions and close positions in time.

4. ** Backtest and Optimization ** :

- Use historical data to backtest strategies to evaluate Sharpe ratios, maximum retracements, and win rates.

- Optimize parameters such as EMA period and ATR threshold to improve policy performance.

---

### Precautions

- ** Trading costs ** : Highly volatile markets may result in frequent trading, and the impact of fees and slippage on earnings needs to be considered.

- ** Risk Control ** : Aggressive strategies may face large retracements and need to strictly implement stop losses.

- ** Scalability ** : Additional metrics (such as volume or VIX) can be added to enhance strategy robustness, or combined with machine learning to predict trends and volatility.

---

### Summary

This is a trend following strategy based on dual moving averages and ATR, designed for volatile high IV markets. By entering into high volatility and exiting into low volatility, the strategy combines aggressive and risk-adjusted returns for traders seeking a high sharpe ratio. It is recommended to fully backtest before implementation and adjust the parameters according to the specific market.

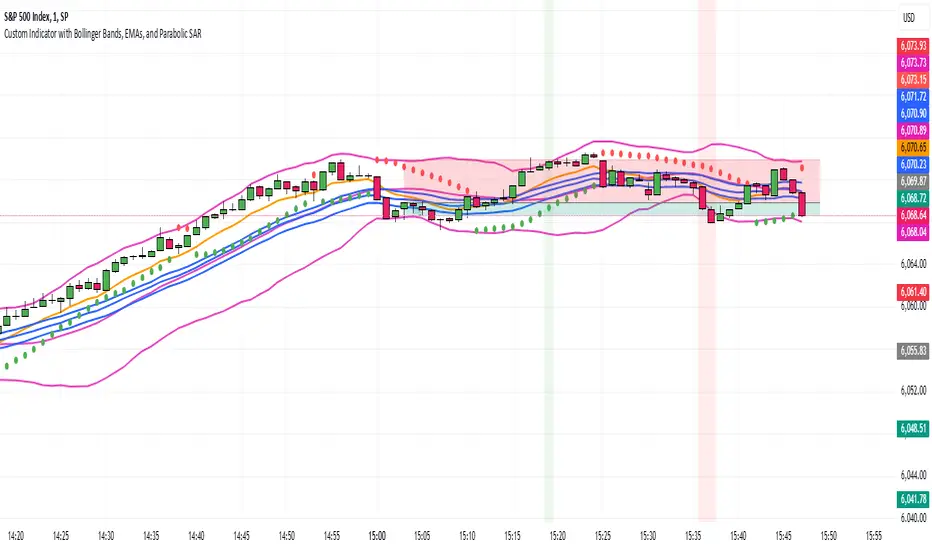

Jumbalika BandsThis indicator is designed using several common technical analysis tools: Bollinger Bands, Exponential Moving Averages (EMAs), and the Parabolic SAR. I'll walk you through each section to explain how it works and how you can use it:

1. Bollinger Bands

Bollinger Bands are used to measure volatility and overbought/oversold conditions. It consists of three lines:

Basis (Middle Line): A simple moving average (SMA) of the price over a defined period (in this case, 20 periods).

Upper Band: The basis plus a certain number of standard deviations. It represents the upper boundary of expected price movement.

Lower Band: The basis minus the same number of standard deviations. It represents the lower boundary of expected price movement.

Interpretation:

Overbought: If the price moves above the upper band, it could signal that the asset is overbought.

Oversold: If the price moves below the lower band, it could signal that the asset is oversold.

Volatility: A wider band indicates higher volatility, and a narrower band indicates lower volatility.

2. Exponential Moving Averages (EMAs)

The indicator plots four different EMAs:

9-period EMA: This is a short-term trend indicator.

20-period EMA on Close: This is another medium-term trend indicator, based on the close price.

20-period EMA on High: A variation of the 20-period EMA, but based on the high prices.

20-period EMA on Low: A variation of the 20-period EMA, but based on the low prices.

Interpretation:

9 EMA: A faster-moving average that responds quicker to price changes. It can be used to identify short-term trends.

20 EMA: A slower-moving average that reacts more gradually to price changes. It helps identify the broader trend.

High/Low EMAs: These give additional insights into the extremes of price action, which can help identify possible support or resistance levels.

Trading signals (common usage):

Crossover: When a shorter EMA (like the 9 EMA) crosses above a longer EMA (like the 20 EMA), it could be a bullish signal. When it crosses below, it could be a bearish signal.

3. Parabolic SAR

The Parabolic SAR is a trend-following indicator that is used to identify potential price reversals. The Parabolic SAR is plotted as a series of dots either above or below the price, depending on the trend:

Below the price: The trend is up (bullish).

Above the price: The trend is down (bearish)

4. Background Coloring (Optional)

The background will change color when the price crosses the Bollinger Bands:

Green background when the price is above the upper Bollinger Band.

Red background when the price is below the lower Bollinger Band.

Adjust the values for Bollinger Bands, EMAs, and Parabolic SAR directly in the indicator settings to suit your trading preferences.

Bollinger Bands: If the price is above the upper band, it might indicate an overbought condition, while if it's below the lower band, it might indicate an oversold condition.

EMAs: The 9 EMA is often used to track short-term trends, while the 20-period EMAs (on the close, high, and low) help analyze the broader market trend.

Parabolic SAR: The Parabolic SAR is often used to identify trend reversals. If the SAR is below the price, the trend is up, and if it's above the price, the trend is down.

Background Color: The background coloring helps visually highlight potential market conditions when the price breaks out of the Bollinger Bands.

Example Use Case:

Decide the trend based on the parabolic SAR, when the bar touches the upper or lower Bollinger take a short or long position based on the price action using EMAs.

EMA Crossover with RSI and DistanceEMA Crossover with RSI and Distance Strategy

This strategy combines Exponential Moving Averages (EMA) with Relative Strength Index (RSI) and distance-based conditions to generate buy, sell, and neutral signals. It is designed to help traders identify entry and exit points based on multiple technical indicators.

Key Components:

Exponential Moving Averages (EMA):

The strategy uses four EMAs: EMA 5, EMA 13, EMA 40, and EMA 55.

A buy signal (long) is triggered when EMA 5 crosses above EMA 13 and EMA 40 crosses above EMA 55.

A sell signal (short) is generated when EMA 55 crosses above EMA 40.

The distance between EMAs (5 and 13) is also important. If the current distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, a neutral condition is triggered, preventing a signal even if all other conditions are met.

Relative Strength Index (RSI):

The 14-period RSI is used to determine market strength and direction.

The strategy requires RSI to be above 50 and greater than the average RSI (over the past 14 periods) for a buy signal.

If the RSI is above 60, a green signal is given, indicating a strong bullish condition, even if the EMA conditions are not fully met.

If the RSI is below 40, a red signal is given, indicating a strong bearish condition, regardless of the EMA crossover.

Distance Conditions:

The strategy calculates the distance between EMA 5 and EMA 13 on each candle and compares it to the average distance of the last 5 candles.

If the current distance between EMA 5 and EMA 13 is lower than the average of the last 5 candles, a neutral signal is triggered. This helps avoid entering a trade when the market is losing momentum.

Additionally, if the distance between EMA 40 and EMA 13 is greater than the previous distance, the previous signal is kept intact, ensuring that the trend is still strong enough for the signal to remain valid.

Signal Persistence:

Once a buy (green) or sell (red) signal is triggered, it remains intact as long as the price is closing above EMA 5 for long trades or below EMA 55 for short trades.

If the price moves below EMA 5 for long trades or above EMA 55 for short trades, the signal is recalculated based on the most recent conditions.

Signal Display:

Green Signals: Represent a strong buy signal and are shown below the candle when the RSI is above 60.

Red Signals: Represent a strong sell signal and are shown above the candle when the RSI is below 40.

Neutral Signals: Displayed when the conditions for entry are not met, specifically when the EMA distance condition is violated.

Long and Short Signals: Additional signals are shown based on the EMA crossovers and RSI conditions. These signals are plotted below the candle for long positions and above the candle for short positions.

Trade Logic:

Long Entry: Enter a long trade when EMA 5 crosses above EMA 13, EMA 40 crosses above EMA 55, and the RSI is above 50 and greater than the average RSI. Additionally, the current distance between EMA 5 and EMA 13 should be larger than the average distance of the last 5 candles.

Short Entry: Enter a short trade when EMA 55 crosses above EMA 40 and the RSI is below 40.

Neutral Condition: If the distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, the strategy will not trigger a signal, even if other conditions are met.

Refined SMA/EMA Crossover with Ichimoku and 200 SMA FilterYour **Refined SMA/EMA Crossover with Ichimoku and 200 SMA Filter** strategy is a multi-faceted technical trading strategy that combines several key technical indicators to refine entry and exit points for trades. Here's a breakdown of the components and how they work together:

### 1. **SMA/EMA Crossover**

- **Simple Moving Average (SMA) & Exponential Moving Average (EMA) Crossover**:

- The core idea behind the crossover strategy is to use the relationship between two moving averages to generate buy or sell signals.

- **SMA** (Simple Moving Average) gives an average of past prices over a set period.

- **EMA** (Exponential Moving Average) places more weight on recent prices, making it more responsive to price movements.

- A **bullish crossover** occurs when a shorter period moving average (such as a 50-period EMA) crosses above a longer period moving average (such as a 200-period SMA), signaling a potential buy.

- A **bearish crossover** occurs when a shorter period moving average crosses below the longer period moving average, signaling a potential sell.

### 2. **Ichimoku Cloud**

- The **Ichimoku Cloud** is a versatile indicator that provides insight into trend direction, support and resistance levels, and momentum.

- **Cloud (Kumo)**: The space between the Senkou Span A and Senkou Span B lines. It helps identify whether the market is in an uptrend, downtrend, or consolidation.

- **Tenkan-sen** (Conversion Line) and **Kijun-sen** (Base Line): These lines are used for additional confirmation of trend direction.

- **Chikou Span**: A lagging line that is used to confirm the trend.

- The general trading rules based on the Ichimoku Cloud are:

- **Bullish Signal**: When the price is above the cloud and the Tenkan-sen crosses above the Kijun-sen.

- **Bearish Signal**: When the price is below the cloud and the Tenkan-sen crosses below the Kijun-sen.

### 3. **200 SMA Filter**

- The **200 SMA Filter** serves as a long-term trend filter.

- When the price is **above the 200 SMA**, it signals a long-term bullish trend, and you only look for buying opportunities.

- When the price is **below the 200 SMA**, it signals a long-term bearish trend, and you only look for selling opportunities.

- This filter helps to avoid counter-trend trades, aligning your positions with the broader market trend.

### **How the Strategy Works Together**

- **Trade Setup (Long Position)**

1. The **200 SMA Filter** must confirm an **uptrend** by ensuring that the price is above the 200 SMA.

2. A **bullish crossover** (e.g., the 50 EMA crossing above the 200 SMA) occurs.

3. **Ichimoku Cloud** confirms a bullish trend, with the price above the cloud and the Tenkan-sen crossing above the Kijun-sen.

4. You enter a **long trade** with this confluence of signals.

- **Trade Setup (Short Position)**

1. The **200 SMA Filter** must confirm a **downtrend** by ensuring the price is below the 200 SMA.

2. A **bearish crossover** (e.g., the 50 EMA crossing below the 200 SMA) occurs.

3. **Ichimoku Cloud** confirms a bearish trend, with the price below the cloud and the Tenkan-sen crossing below the Kijun-sen.

4. You enter a **short trade** with this confluence of signals.

### **Exit Strategy**

- Exits can be determined based on any of the following:

- **SMA/EMA crossover reversal**: Exit when the shorter-term moving average crosses back below the longer-term moving average for a long position or crosses above for a short position.

- **Ichimoku Cloud reversal**: If the price breaks through the cloud or the Tenkan-sen and Kijun-sen lines cross in the opposite direction.

- **Profit target or stop loss**: Setting predefined profit targets or using a trailing stop to lock in profits as the trade moves in your favor.

Summary of the Strategy

This strategy is designed to identify strong trends and avoid false signals by combining:

SMA/EMA crossovers for immediate market direction signals.

Ichimoku Cloud for confirming the strength and trend direction.

A 200

SMA filter to ensure trades align with the long-term trend.

By using these multiple indicators together, the strategy aims to refine entry and exit points, minimize risk, and increase the likelihood of successful trades.

MultiLayer Awesome Oscillator Saucer Strategy [Skyrexio]Overview

MultiLayer Awesome Oscillator Saucer Strategy leverages the combination of Awesome Oscillator (AO), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Awesome Oscillator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Awesome Oscillator shall create the "Saucer" long signal (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created "Saucer signal".

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one "Saucer" signal another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's go through all concepts used in this strategy to understand how they works together. Let's start from the easies one, the EMA. Let's briefly explain what is EMA. The Exponential Moving Average (EMA) is a type of moving average that gives more weight to recent prices, making it more responsive to current price changes compared to the Simple Moving Average (SMA). It is commonly used in technical analysis to identify trends and generate buy or sell signals. It can be calculated with the following steps:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy uses EMA an initial long term trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

Let's go to the next, short-term trend filter which consists of Alligator and Fractals. Let's briefly explain what do these indicators means. The Williams Alligator, developed by Bill Williams, is a technical indicator designed to spot trends and potential market reversals. It uses three smoothed moving averages, referred to as the jaw, teeth, and lips:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When these lines diverge and are properly aligned, the "alligator" is considered "awake," signaling a strong trend. Conversely, when the lines overlap or intertwine, the "alligator" is "asleep," indicating a range-bound or sideways market. This indicator assists traders in identifying when to act on or avoid trades.

The Williams Fractals, another tool introduced by Bill Williams, are used to pinpoint potential reversal points on a price chart. A fractal forms when there are at least five consecutive bars, with the middle bar displaying the highest high (for an up fractal) or the lowest low (for a down fractal), relative to the two bars on either side.

Key Points:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often combine fractals with other indicators to confirm trends or reversals, improving the accuracy of trading decisions.

How we use their combination in this strategy? Let’s consider an uptrend example. A breakout above an up fractal can be interpreted as a bullish signal, indicating a high likelihood that an uptrend is beginning. Here's the reasoning: an up fractal represents a potential shift in market behavior. When the fractal forms, it reflects a pullback caused by traders selling, creating a temporary high. However, if the price manages to return to that fractal’s high and break through it, it suggests the market has "changed its mind" and a bullish trend is likely emerging.

The moment of the breakout marks the potential transition to an uptrend. It’s crucial to note that this breakout must occur above the Alligator's teeth line. If it happens below, the breakout isn’t valid, and the downtrend may still persist. The same logic applies inversely for down fractals in a downtrend scenario.

So, if last up fractal breakout was higher, than Alligator's teeth and it happened after last down fractal breakdown below teeth, algorithm considered current trend as an uptrend. During this uptrend long trades can be opened if signal was flashed. If during the uptrend price breaks down the down fractal below teeth line, strategy considered that uptrend is finished with the high probability and strategy closes all current long trades. This combination is used as a short term trend filter increasing the probability of opening profitable long trades in addition to EMA filter, described above.

Now let's talk about Awesome Oscillator's "Sauser" signals. Briefly explain what is the Awesome Oscillator. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

Now we know what is AO, but what is the "Saucer" signal? This concept was introduced by Bill Williams, let's briefly explain it and how it's used by this strategy. Initially, this type of signal is a combination of the following AO bars: we need 3 bars in a row, the first one shall be higher than the second, the third bar also shall be higher, than second. All three bars shall be above the zero line of AO. The price bar, which corresponds to third "saucer's" bar is our signal bar. Strategy places buy stop order one tick above the price bar which corresponds to signal bar.

After that we can have the following scenarios.

Price hit the order on the next candle in this case strategy opened long with this price.

Price doesn't hit the order price, the next candle set lower low. If current AO bar is increasing buy stop order changes by the script to the high of this new bar plus one tick. This procedure repeats until price finally hit buy order or current AO bar become decreasing. In the second case buy order cancelled and strategy wait for the next "Saucer" signal.

If long trades has been opened strategy use all the next signals until number of trades doesn't exceed 5. All trades are closed when the trend changes to downtrend according to combination of Alligator and Fractals described above.

Why we use "Saucer" signals? If AO above the zero line there is a high probability that price now is in uptrend if we take into account our two trend filters. When we see the decreasing bars on AO and it's above zero it's likely can be considered as a pullback on the uptrend. When we see the stop of AO decreasing and the first increasing bar has been printed there is a high probability that this local pull back is finished and strategy open long trade in the likely direction of a main trend.

Why strategy use only 10% per signal? Sometimes we can see the false signals which appears on sideways. Not risking that much script use only 10% per signal. If the first long trade has been open and price continue going up and our trend approximation by Alligator and Fractals is uptrend, strategy add another one 10% of capital to every next saucer signal while number of active trades no more than 5. This capital allocation allows to take part in long trades when current uptrend is likely to be strong and use only 10% of capital when there is a high probability of sideways.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.11.25. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 10%

Maximum Single Position Loss: -5.10%

Maximum Single Profit: +22.80%

Net Profit: +2838.58 USDT (+28.39%)

Total Trades: 107 (42.99% win rate)

Profit Factor: 3.364

Maximum Accumulated Loss: 373.43 USDT (-2.98%)

Average Profit per Trade: 26.53 USDT (+2.40%)

Average Trade Duration: 78 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 3h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Multi-Timeframe MACD, Signal & Histogram TableThis Pine Script is designed for the TradingView platform to create a multi-timeframe MACD (Moving Average Convergence Divergence), Signal, and Histogram table that displays values for different timeframes. The script uses the MACD indicator to assess market trends across various timeframes and display the results in a table format on the chart. Here's a breakdown of its components and functionality:

1. User Inputs for Timeframes:

The script allows the user to input five different timeframes for the analysis. These are configured using input.string, which enables the user to select from a list of timeframes (from seconds to months).

tf1 to tf5 represent the different timeframes (for example, 5 minutes, 15 minutes, 60 minutes, 240 minutes, and daily).

2. MACD Settings:

The script provides adjustable settings for the MACD calculation:

macdShortLength (default 12): The length of the short-term moving average for the MACD.

macdLongLength (default 26): The length of the long-term moving average for the MACD.

macdSignalLength (default 9): The length of the signal line, which is an EMA (Exponential Moving Average) of the MACD line.

3. MACD Calculation Function (calc_macd):

This function calculates the MACD, Signal, and Histogram values:

MACD Line: Difference between the fast and slow exponential moving averages.

Signal Line: EMA of the MACD line.

Histogram: Difference between the MACD line and Signal line.

4. Requesting Multi-Timeframe Data:

The script calculates the MACD, Signal, and Histogram for the selected timeframes (tf1 to tf5) using request.security, which retrieves data for those timeframes:

macd_tf1, signal_tf1, hist_tf1 for Timeframe 1 (and similar variables for the other timeframes).

5. Rounding Values: